Ask The Experts

We Maximize Your Social Security!

We Maximize Your Social Security!

We Show You How to Make The Best Choices

Speak to An Expert: Access to A Dedicated Social Security Advisor

Tell You When to File, What to File, & How to File

Give You a Personalized Social Security Strategy With Step-By-Step Instructions

Compare & Contrast Scenarios

Easy Visuals of Monthly, Annual, & Total Benefits

Help You With Filing Questions

We Make It Easy!

All THIS included in your personalized Maximum Social Security StrategySM!

Evaluate Your Options

Did you know that there are literally thousands of Social Security options for most couples? Choosing when and how to file for Social Security is very confusing and potentially very costly if the wrong decisions are made. Until now, Social Security has been thought of as an "automatic" benefit with most individuals and couples simply signing-up as soon as they reached 62. This is changing and for good reason; smart retirees are evaluating their options to make sure that they maximize their Social Security and don't leave money on the table. Make sure that you're making the best decisions possible regarding this important retirement asset. There is some important educational material below; get your Maximum Social Security StrategySM today!

- Benefits on Your Own Record

- Singles generally have more Social Security options available to them than is immediately apparent and as such, it is important to plan carefully. There are some very unique Social Security StrategiesSM available to singles that most singles are not even aware of. Which strategies may be available to you will depend on your specific circumstances.

Maximizing Social Security is especially important for singles given that single individuals are generally more dependent on a single earnings record and investment portfolio, yet have retirement expenses that are well over half of those of a couple in similar circumstances. Importantly, many singles don't realize that they may be subject to dual entitlement (i.e., being entitled on someone else's earnings record and also on their own earnings record).

Retirement Benefits on Your Own Record:

- Life expectancy is an especially critical consideration for singles.

- Accurately determining when to claim benefits is extremely important for singles.

- Generally speaking, you can claim retirement benefits on your own record as early 62. If you do, your benefits will be reduced by as much as 25% because you elected to claim benefits prior to your Full Retirement Age.

- If you wait to claim benefits until your Full Retirement Age, you will receive 100% of your Primary Insurance Amount.

- Due to Delayed Retirement credits, claiming benefits after your Full Retirement Age can increase your benefits by up to 32% by age 70.

- When deciding when to begin receiving your Social Security benefits, many factors must be taken into account, including, but not limited to: life expectancy, general health, marital status (and previous marital status), work status, tax status, and your overall financial circumstances and lifestyle objectives.

- Think you may have made a mistake? Even if you have already claimed benefits, there may be a way to start over. Give us a call to discuss this further.

According to the Center for Retirement Research at Boston College, many individuals and couples make suboptimal choices when deciding how and when to collect their Social Security benefits, resulting in over $25 billion per year in lost retirement benefits. Let us help you make sure that you are not one of them. Call us today to speak with a Social Security Advisor and ask about our Maximum Social Security GuaranteeSM.

- Spousal Benefits

- For married couples, the complex choices surrounding Social Security decisions are especially significant because couples generally have even more options than other beneficiaries. For most couples, there are at least 9,216 different combinations of options! Are you sure you know which combination is right for you?

Deciding which spouse should file first, how long to delay filing for benefits, and which combination of choices is best requires detailed planning and careful consideration in order to ensure that you maximize your Social Security. Furthermore, all decisions are unique to your specific financial circumstances, work status, projected longevity, and overall lifestyle objectives, just to name a few factors. There are many different strategies available to married couples and it is important to select the optimal strategy or combination of strategies.

Spousal Benefits:

- A spousal benefit is a benefit available to one spouse based on the other spouse's earnings record.

- You must be at least 62 to begin collecting a spousal benefit and you cannot collect a spousal benefit until your spouse has filed for benefits on his or her own earnings record.

- If you have your own earnings record, you can claim benefits on your own record or you can collect a spousal benefit worth up to 50% of your spouse’s Primary Insurance Amount (PIA). You are eligible for the higher of the two, but not both.

- Whether to collect a spousal benefit is an important decision in and of itself. If the answer is yes, deciding when to do so is a critical factor to consider. Claiming a spousal benefit prior to Full Retirement Age (FRA) will result in a reduced monthly spousal benefit. However, married couples should seek to identify the Maximum Social Security StrategySM that optimizes their combined benefits while taking into account their overall objectives and special considerations.

Which Social Security strategy is right for you? Again, it highly depends on your specific circumstances as a couple. It may be best to speak with one of our experts. Call today and your Social Security Advisor will help you get started.

- Survivors Benefits

- Survivors benefits are an important source of financial security for millions of Americans. Maximizing survivors benefits is key to protecting yourself against outliving your assets. Making the right decisions regarding survivors benefits, however, is often challenging as there are many options available. Further complicating matters is the fact that the selection of survivors benefits is often impacted by other objectives and variables including dual entitlement (i.e., being entitled as a survivor and also on your own earnings record).

Survivors Benefits:

In the event of the death of a covered worker, several different types of beneficiaries may qualify to receive a survivors benefit based on the earnings record of the worker:

• Widow or Widowers

- In many cases, the widow(er) has dual Social Security entitlement: entitlement based on his or her own earnings record as well as entitlement based on the earnings record of his or her deceased spouse. The survivor can qualify for full survivors benefits after reaching Full Retirement Age (FRA) or he or she can choose to receive reduced survivors benefits as early as age 60. A disabled widow(er) can begin receiving survivors benefits as early as age 50.

Because many widow(ers) have dual entitlement, this means there are options. Where there are options there is complexity and Social Security survivors benefits are no different. Among other considerations, as a survivor you need to be confident that you are claiming benefits on the correct record and at the correct time. Furthermore, there are a variety of combinations of Social Security strategies that can be employed to maximize your Social Security for those that have dual entitlement (i.e. most people).

• Divorced Widow or Widowers

- In many cases, a divorced widow(er) has dual Social Security entitlement: entitlement based on his or her own earnings record as well as entitlement based on the earnings record of his or her deceased divorced spouse. Generally speaking, the survivor can qualify for full survivors benefits after reaching Full Retirement Age (FRA) or he or she can choose to receive reduced survivors benefits as early as age 60. A disabled widow(er) can begin receiving survivors benefits as early as age 50.

It is important to note that to qualify for divorced survivors benefits, you must have been married to the covered worker for at least 10 years and you must not have remarried before age 60.

In addition to dual entitlement, divorced widow(er)s often have even more options available and choices to make when compared to married widow(er)s. Where there are options, there is complexity and Social Security survivors benefits for divorced widow(er)s are no different. Among other considerations, as a survivor, you need to be confident that you are claiming benefits on the correct record and at the correct time.

Furthermore, there are a variety of combinations of Social Security strategies that can be employed to maximize your Social Security for those that have dual entitlement (i.e. most people).

• Minor Children

- When minor children are left behind as survivors, it is absolutely critical to make the right choices to ensure that they receive all of the Social Security survivors benefits and financial protection that they may be entitled to.

Benefit selections and the associated Social Security strategies are complex and need to take into consideration many factors including, but not limited to: the child(ren)'s age(s), care provider(s), medical condition, and the overall circumstances and objectives of the rest of the family.

There are a variety of options available to maximize Social Security for minor children as survivors and those that care for them; call today to speak with a Social Security Advisor for details.

• Dependent Parents

- Even dependent parents may qualify for survivors benefits; call today to speak with a Social Security Advisor for details.

- In many cases, the widow(er) has dual Social Security entitlement: entitlement based on his or her own earnings record as well as entitlement based on the earnings record of his or her deceased spouse. The survivor can qualify for full survivors benefits after reaching Full Retirement Age (FRA) or he or she can choose to receive reduced survivors benefits as early as age 60. A disabled widow(er) can begin receiving survivors benefits as early as age 50.

- Divorce & Social Security

- Divorced spousal benefits are an important source of financial security for millions of Americans. Increasingly, more and more couples are parting ways and protecting yourself and ensuring your financial security by maximizing your Social Security is essential if you find yourself in this situation. Making the right decisions regarding divorced spousal benefits, however, is often challenging as there are many options available. Further complicating matters is the fact that the selection of divorced spousal benefits is often impacted by other objectives and variables including dual entitlement (i.e., being entitled as a divorced spouse and also on your own earnings record).

Divorced Spousal Benefits:

- A divorced spousal benefit is a benefit that may be available to a divorced spouse based on the former spouse's earnings record.

- You must be at least 62 to begin collecting a divorced spousal benefit.

- You must have been married to your former spouse for at least 10 years.

- You must currently be unmarried.

- If you have been married and divorced more than once, you may be eligible for benefits based on more than one earnings record. Selecting which record on which to file a claim is an important and potentially complicated decision.

- You may be able to qualify for divorced spousal benefits even if your former spouse is remarried.

- If you have your own earnings record, you can claim benefits on your own record or you can collect a divorced spousal benefit worth up to 50% of your former spouse’s Primary Insurance Amount (PIA). You are eligible for the higher of the two, but not both combined. As a divorced spouse however, there may be a Social Security strategy available to you that may allow you to file for benefits on both your earnings record as well as your former spouse's earnings record at different times in order to maximize your Social Security.

- Whether to collect a divorced spousal benefit is an important decision in and of itself. If the answer is yes, deciding when to do so is a critical factor to consider. Claiming a divorced spousal benefit prior to Full Retirement Age (FRA) will result in a reduced monthly divorced spousal benefit. However, for most divorced spouses, there are Social Security strategies that are available that combine claims on the records of both spouses in order to maximize your Social Security while taking into account your overall objectives and special considerations.

Which Social Security strategy is right for you? It highly depends on your specific circumstances. It may be best to speak with one of our experts. Call today and your Social Security Advisor will help you get started.

- Taxation of Social Security Benefits

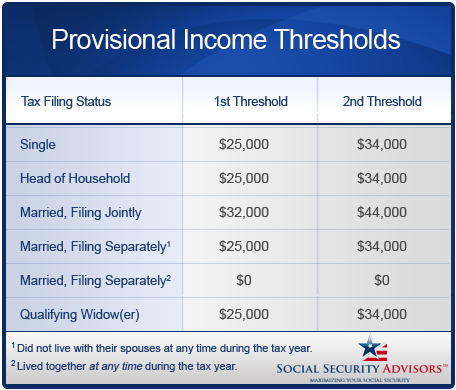

- Most people are not familiar with the effects of taxation on Social Security benefits. This can be harmful because without proper planning, taxation can reduce Social Security benefits by up to 30% in some cases! This is called the Social Security Tax Torpedo and should be avoided whenever possible. Whether or not your Social Security income is subject to taxation depends on the level of your Provisional Income. Provisional Income is defined as follows:

Provisional Income = Modified Adjusted Gross Income + Tax-Exempt Interest + 50% of Your Social Security Benefits

The Provisional Income formula (also known as the Combined Income formula) determines how much of a retiree's Social Security benefits are subject to taxation. Up to the thresholds listed below, Social Security benefits are tax-free. Once the first threshold is reached, up to 50% of Social Security benefits are subject to taxation. Once the second threshold is reached, up to 85% of Social Security benefits will be taxed. Listed below are the current first and second threshold limits, respectively:

Ironically, even though the Social Security Tax Torpedo hits many retirees very hard, few professional advisors have done much to avoid it...until now; at Social Security AdvisorsSM we deal with this head-on.

Social Security income and 401(k)/IRA income are taxed differently which presents opportunities for smart tax planning. At Social Security AdvisorsSM our expert advisors recognize that minimizing the impact of taxation on your Social Security income is critical when seeking to maximize your Social Security and we have developed tax-smart strategies to help you keep as much of your Social Security benefits as possible on an after-tax basis...after all, you've earned it!

Are you confident that you are receiving your Social Security benefits in the most tax-efficient manner possible? It may be best to speak with one of our experts. Call today and your Social Security Advisor will help you get started.

- Pensions from Work Not Subject to Social Security Taxes

- If you work (or have worked) for an employer who does not withhold Social Security taxes from your salary, such as a government agency or an employer in another country, the pension you get based on that work may reduce your Social Security benefits. In addition, Social Security benefits for the spouse of a worker covered by a retirement system other than Social Security may be offset by pension benefits. These Social Security offsets described above are provisions of the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO).

Windfall Elimination Provision:

- The Windfall Elimination Provision primarily affects you if you earned a pension in any job where you did not pay Social Security taxes and you also worked in other jobs long enough to qualify for a Social Security retirement or disability benefit.

- Prior to the implementation of the Windfall Elimination Provision (or WEP) in 1983, retirees receiving pensions from jobs in which they had not contributed to Social Security could still claim significant Social Security benefits. Most of these individuals were police officers, fire fighters, teachers, or employees of federal, state, or local government agencies. This was deemed to be unfair and thus the Windfall Elimination Provision was introduced to "restore a level playing field."

- The Windfall Elimination Provision is meant to reduce Social Security benefits for individuals who receive retirement benefits from a retirement system other than Social Security.

To read more about the Windfall Elimination Provision visit: More About The Windfall Elimination Provision

Government Pension Offset:

- The Government Pension Offset applies to spousal or survivors benefits for widow(er)s.

- If you receive a pension from a federal, state or local government based on work where you did not pay Social Security taxes, your Social Security spousal benefits or survivors benefits may be reduced by the Government Pension Offset. Your Social Security benefits will be reduced by two-thirds of your government pension. In other words, if you get a monthly civil service pension of $600, two-thirds of that, or $400, must be deducted from your Social Security benefits. For example, if you are eligible for a $500 spouse's or widow(er)'s benefit from Social Security, you will receive $100 per month from Social Security ($500 – $400 = $100).

- In enacting the Government Pension Offset provision, Congress intended to ensure that when determining the amount of a spousal benefit, government employees who do not pay Social Security taxes would be treated in a similar manner to those who work in the private sector and do pay Social Security taxes.

To read more about the Government Pension Offset visit: More About the Government Pension Offset

Social Security decisions are complicated enough without having to think of extra provisions and offsets which can be very confusing. As the Social Security experts, you may find it helpful to speak with one of our advisors regarding your specific circumstances and objectives. Call us today to get started. And don't forget, our service is always backed by our Maximum Social Security GuaranteeSM.

View Pricing Plans